How to Avoid PMI on a Conventional Loan in 2025

Image Source: pexels

Private Mortgage Insurance (PMI) can add significant costs to a homeowner’s budget. Monthly PMI fees often range from $167 to $500 for a $400,000 mortgage. Avoiding PMI saves money and reduces financial stress. Strategies like piggyback loans or lender-paid PMI offer practical solutions for those wondering how to avoid PMI on a conventional loan.

Key Takeaways

- Making a 20% down payment is the simplest way to avoid PMI. This saves money and reduces monthly payments.

- Consider a piggyback loan if you can’t afford a full 20% down payment. This option allows you to take two loans to meet the equity requirement.

- Explore no-PMI loan programs offered by some lenders. These programs help first-time buyers avoid PMI without needing a second mortgage.

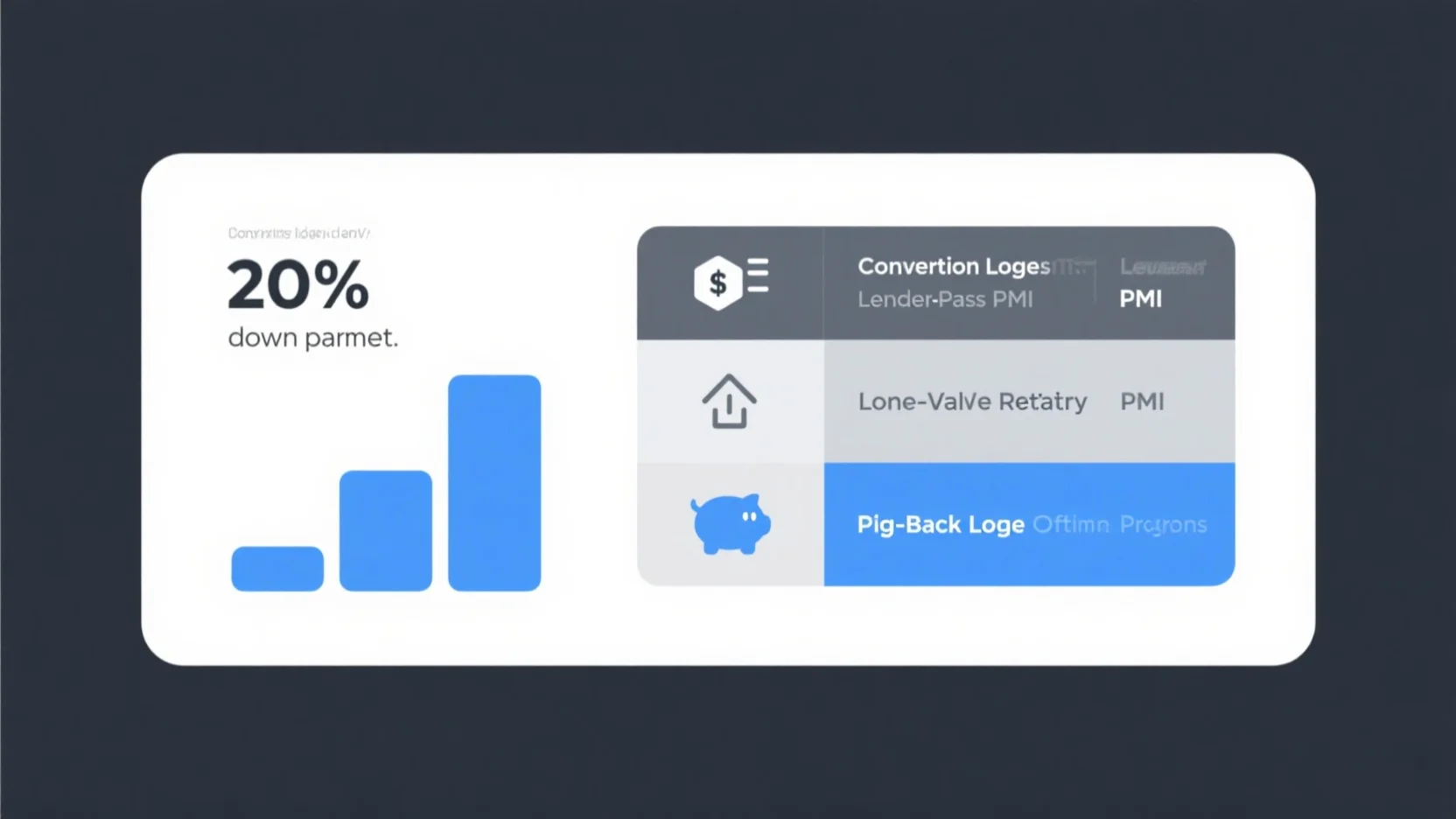

How to Avoid PMI on a Conventional Loan

Image Source: pexels

Make a 20% Down Payment

The most straightforward way to avoid PMI is by making a 20% down payment. This approach eliminates the need for private mortgage insurance entirely, as lenders consider loans with 20% equity less risky. For example, on a $300,000 home, a buyer would need to provide $60,000 upfront. While this option requires significant savings, it offers long-term financial benefits by reducing monthly payments and avoiding PMI costs altogether.

Use a Piggyback Loan (80-10-10 Loan)

A piggyback loan, also known as an 80-10-10 loan, is an effective strategy for those who cannot afford a full 20% down payment. This method involves taking out two loans: the first covers 80% of the home’s value, the second covers 10%, and the buyer provides the remaining 10% as a down payment.

- Steps to use a piggyback loan :

- Secure approval for both loans.

- Complete the underwriting process.

- Conduct a home appraisal and inspection.

- Prepare funds for the down payment and closing costs.

- Respond promptly to lender requests.

For instance, on a $200,000 home, the buyer would take out a $160,000 primary mortgage, a $20,000 second mortgage, and pay $20,000 upfront. This structure avoids PMI by meeting the 20% equity requirement. However, second mortgages often have higher interest rates, which should be factored into the decision.

Opt for Lender-Paid PMI

Lender-paid PMI (LPMI) shifts the cost of PMI into the loan’s interest rate. While this increases the interest rate slightly—typically by 0.25%—it eliminates the separate PMI payment. For a $300,000 home with a 10% down payment, LPMI might result in a monthly payment of $1,796 compared to $1,751 without LPMI.

- Advantages of LPMI :

- Lower monthly payments.

- Fixed monthly costs.

- Higher chances of loan approval.

- Potential tax deductibility.

- Disadvantages of LPMI :

- Permanence of the higher interest rate.

- Limited availability.

- Potentially higher long-term costs.

This option works well for buyers who plan to stay in their homes long-term and prefer predictable monthly payments.

Explore No-PMI Loan Programs

Some lenders offer no-PMI loan programs that allow buyers to make low down payments without requiring PMI. These programs often cater to first-time homebuyers or specific professions, such as teachers or healthcare workers. Unlike piggyback loans, no-PMI programs do not involve a second mortgage, simplifying the process. Buyers should research local and state programs that provide grants or down payment assistance to help avoid PMI.

Consider VA Loans for Military Members

VA loans are a top choice for eligible veterans and active-duty service members. These loans eliminate PMI entirely, making homeownership more affordable. Additionally, VA loans offer 100% financing, meaning no down payment is required. While they include a one-time funding fee, this cost can be rolled into the loan amount, avoiding ongoing expenses like PMI. Veterans who used VA loans last year saved over $40 billion in PMI costs, highlighting the significant financial advantages of this option.

What Is PMI and Why Is It Required?

Definition and Purpose of PMI

Private Mortgage Insurance (PMI) is a type of insurance that protects lenders if borrowers fail to repay their loans. Lenders require PMI when buyers make a down payment of less than 20%. This insurance reduces the financial risk for lenders by covering a portion of the loan in case of default. PMI enables buyers to purchase homes with smaller down payments, but it adds an extra cost to their monthly mortgage payments.

Tip : Buyers can avoid PMI by exploring strategies like making a larger down payment or using alternative loan programs.

When PMI Is Required on Conventional Loans

PMI is typically required when the down payment is less than 20% of the home’s purchase price. Lenders view smaller down payments as higher risk, which triggers the need for mortgage insurance. Borrowers who provide at least 20% upfront or maintain a loan-to-value (LTV) ratio of 80% or lower are usually exempt from PMI. For example, a buyer purchasing a $300,000 home with a $60,000 down payment would not need PMI, as the LTV ratio would meet the 80% threshold.

How PMI Affects Your Monthly Payments

PMI increases the overall cost of homeownership. The annual cost of PMI typically ranges from 0.5% to 1.5% of the loan amount. For a $400,000 mortgage, PMI fees could range from $2,000 to $6,000 per year, or $167 to $500 per month. These additional costs can strain monthly budgets, making it essential for buyers to explore options on how to avoid PMI on a conventional loan. By reducing or eliminating PMI, buyers can save thousands of dollars over the life of their mortgage.

How to Eliminate PMI After Purchase

Image Source: unsplash

Build Equity Through Regular Payments

Paying your mortgage on time consistently builds equity in your home. Each payment reduces the loan balance, bringing you closer to the 20% equity threshold required to eliminate PMI. Over time, this strategy not only helps you save on PMI costs but also increases your ownership stake in the property. Homeowners who stay disciplined with their payments can achieve this milestone faster than expected.

Make Extra Payments to Reach 20% Equity Faster

Making additional payments toward your principal accelerates equity growth. Even small extra payments can significantly reduce your loan balance over time. For example, adding $100 to your monthly payment on a $250,000 mortgage could save thousands in interest and help you eliminate PMI years earlier. Another effective approach is to use bonuses or tax refunds to make lump-sum payments. These strategies allow homeowners to reach the 20% equity mark more quickly.

Request PMI Cancellation at 80% Loan-to-Value (LTV)

Once your loan-to-value (LTV) ratio reaches 80%, you can formally request PMI cancellation. Start by submitting a written request to your mortgage servicer. Include documentation, such as a recent appraisal, to prove your home’s value. A solid payment history, with no late payments in the past 12 months, strengthens your case. Following these steps ensures a smooth PMI removal process:

- Confirm your LTV ratio has reached 80%.

- Gather necessary documents, including an appraisal if required.

- Submit a written request to your lender.

- Follow up to ensure the cancellation is processed.

Refinance Your Loan to Remove PMI

Refinancing offers another way to eliminate PMI, especially if your home’s value has increased. By refinancing, you can secure a new loan without PMI, provided your equity exceeds 20%. This option also allows you to take advantage of lower interest rates, potentially reducing your monthly payments. However, refinancing comes with upfront costs, such as closing fees, and may reset your loan term. Homeowners should weigh these factors carefully before proceeding. Eliminating PMI through refinancing can save hundreds of dollars monthly, freeing up funds for other financial goals like retirement or debt repayment.

Avoiding PMI offers significant financial benefits. Lower monthly expenses improve cash flow and allow faster equity building. Misconceptions, like PMI being permanent or requiring a 20% down payment, often delay homeownership unnecessarily. Buyers should explore strategies like piggyback loans or no-PMI programs. Consulting a mortgage professional ensures the best financial outcome.

FAQ

What are the benefits of avoiding PMI?

Avoiding PMI reduces monthly mortgage costs, improves cash flow, and accelerates equity building. Buyers can save thousands over the loan term, making homeownership more affordable. 🏡

Can first-time homebuyers avoid PMI?

Yes, many lenders offer no-PMI programs for first-time buyers. These programs often require low down payments and cater to specific professions like teachers or healthcare workers.

Is refinancing always the best way to remove PMI?

Refinancing works well if home values rise or interest rates drop. However, upfront costs like closing fees may outweigh savings. Homeowners should evaluate their financial goals carefully.